Page 190 - FBL AR 2019-20

P. 190

Fermenta Biotech Limited

Annual Report 2019-20

Notes to the Consolidated financial statements for the year ended March 31, 2020

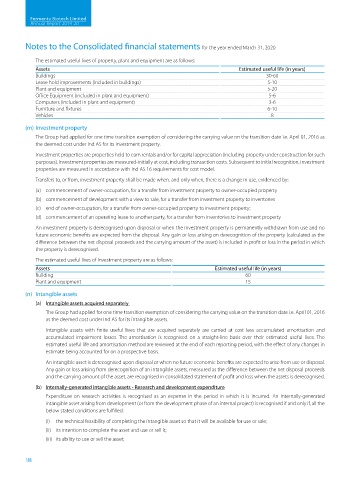

The estimated useful lives of property, plant and equipment are as follows:

Assets Estimated useful life (in years)

Buildings 30-60

Lease hold improvements (included in buildings) 5-10

Plant and equipment 5-20

Office Equipment (included in plant and equipment) 5-6

Computers (included in plant and equipment) 3-6

Furniture and fixtures 6-10

Vehicles 8

(m) Investment property

The Group had applied for one time transition exemption of considering the carrying value on the transition date i.e. April 01, 2016 as

the deemed cost under Ind AS for its investment property.

Investment properties are properties held to earn rentals and/or for capital appreciation (including property under construction for such

purposes). Investment properties are measured-initially at cost, including transaction costs. Subsequent to initial recognition, investment

properties are measured in accordance with Ind AS 16 requirements for cost model.

Transfers to, or from, investment property shall be made when, and only when, there is a change in use, evidenced by:

(a) commencement of owner-occupation, for a transfer from investment property to owner-occupied property

(b) commencement of development with a view to sale, for a transfer from investment property to inventories

(c) end of owner-occupation, for a transfer from owner-occupied property to investment property;

(d) commencement of an operating lease to another party, for a transfer from inventories to investment property

An investment property is derecognised upon disposal or when the investment property is permanently withdrawn from use and no

future economic benefits are expected from the disposal. Any gain or loss arising on derecognition of the property (calculated as the

difference between the net disposal proceeds and the carrying amount of the asset) is included in profit or loss in the period in which

the property is derecognised.

The estimated useful lives of Investment property are as follows:

Assets Estimated useful life (in years)

Building 60

Plant and equipment 15

(n) Intangible assets

(a) Intangible assets acquired separately

The Group had applied for one time transition exemption of considering the carrying value on the transition date i.e. April 01, 2016

as the deemed cost under Ind AS for its intangible assets.

Intangible assets with finite useful lives that are acquired separately are carried at cost less accumulated amortisation and

accumulated impairment losses. The amortisation is recognised on a straight-line basis over their estimated useful lives. The

estimated useful life and amortisation method are reviewed at the end of each reporting period, with the effect of any changes in

estimate being accounted for on a prospective basis.

An intangible asset is derecognised upon disposal or when no future economic benefits are expected to arise from use or disposal.

Any gain or loss arising from derecognition of an intangible assets, measured as the difference between the net disposal proceeds

and the carrying amount of the asset, are recognised in consolidated statement of profit and loss when the assets is derecognised.

(b) Internally-generated intangible assets - Research and development expenditure

Expenditure on research activities is recognised as an expense in the period in which it is incurred. An Internally-generated

intangible asset arising from development (or from the development phase of an internal project) is recognised if and only if, all the

below stated conditions are fulfilled:

(i) the technical feasibility of completing the intangible asset so that it will be available for use or sale;

(ii) its intention to complete the asset and use or sell it;

(iii) its ability to use or sell the asset;

188